Disability vs Workers Compensation: Know the Difference

Many federal workers think they’re fully protected in case of injury or illness. But are they? Two different benefits often cause confusion: disability insurance vs workers compensation. Understanding how they work—and where the gaps are—can protect your income and peace of mind.

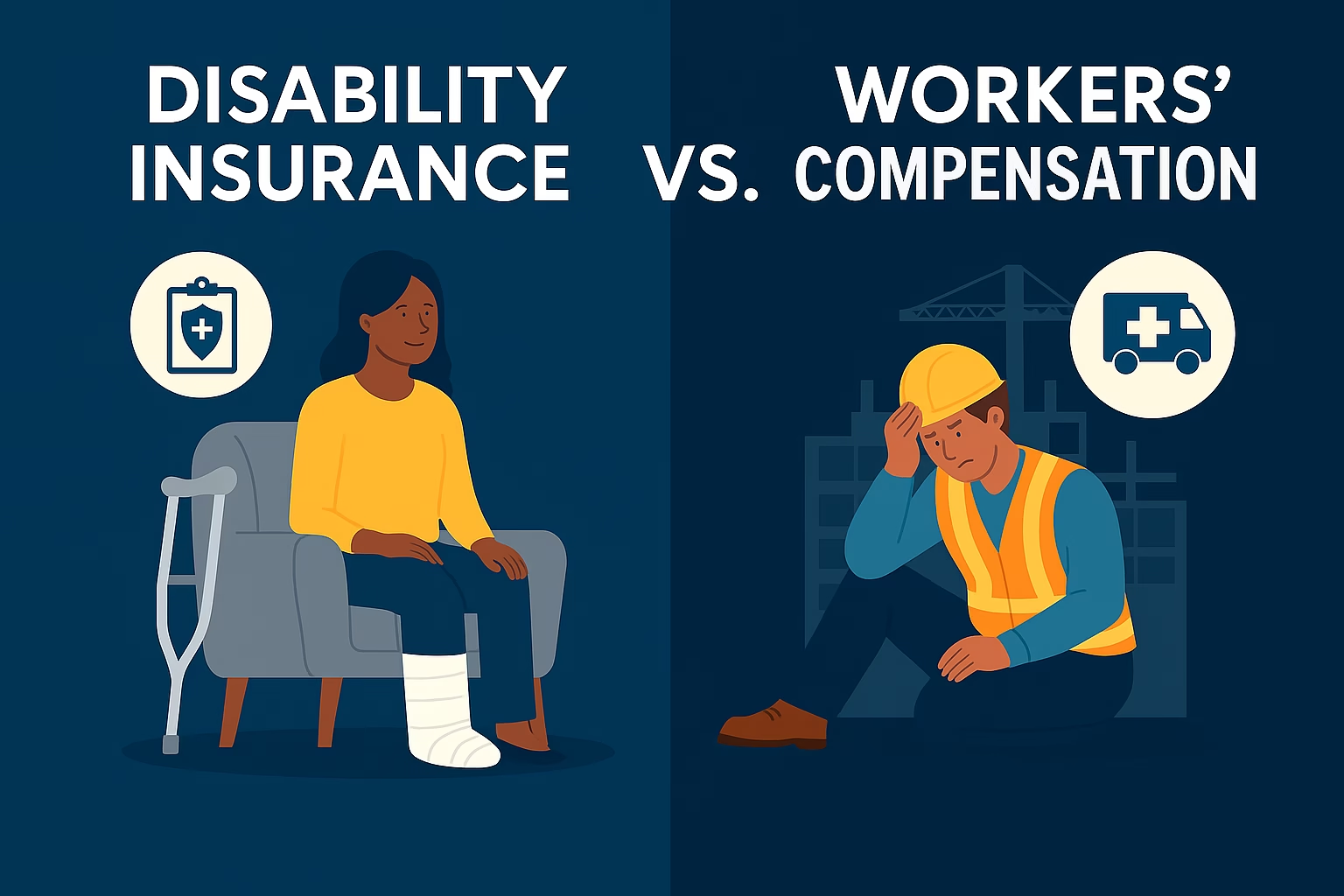

Worker’s Compensation: Limited but Mandatory

Worker’s compensation covers injuries or illnesses that happen while working.

Key features:

- Pays for medical care and partial wages

- Only applies to work-related accidents

- Required by the government

- Managed by the Department of Labor

Example: You fall on the job and break your arm. Worker’s comp pays your medical bills.

Disability Insurance: More Complete Protection

Disability insurance covers income loss, regardless of whether the injury happened on or off the job.

Key features:

- Covers most illnesses, surgeries, or accidents

- Applies even if the incident is unrelated to work

- Optional—you must enroll

- Available as short-term or long-term coverage

Example: You need surgery and can’t work for 8 weeks. Disability insurance fills the gap.

Disability vs Workers Compensation: Comparison

| Feature | Workers Comp | Disability Insurance |

|---|---|---|

| On-the-job injuries | ✅ Yes | ❌ No |

| Off-the-job incidents | ❌ No | ✅ Yes |

| Government-provided | ✅ Yes | ❌ Optional |

| Income replacement | ✅ Partial | ✅ Partial |

| Enrollment | Automatic | Voluntary |

Why You May Need Both

Workers’ compensation only covers you while working.

Disability insurance covers the rest of life’s unexpected moments. Without both, your financial safety net is incomplete.

Final Thought

Now that you understand the key differences in disability vs workers’ compensation, take the next step.

Protect Your Income—Before It’s Too Late

Let us help you choose the right disability plan for your federal career.

👉 Book your free consultation here